uae-bookkeeping.com

Common Bookkeeping Mistakes UAE Businesses Make (and How to Avoid FTA Penalties)

Common Bookkeeping Mistakes UAE Businesses Make (and How to Avoid FTA Penalties)

Gupta Group International

1/22/20263 min read

Common Bookkeeping Mistakes UAE Businesses Make (and How to Avoid FTA Penalties)

In today’s fast-evolving UAE business landscape, maintaining accurate bookkeeping isn’t just good practice — it’s a regulatory requirement. With stringent tax laws, periodic Federal Tax Authority (FTA) audits and stiff penalties for non-compliance, poor bookkeeping can cost businesses thousands in fines, interest charges, and reputational damage.

Whether you operate in Dubai, Abu Dhabi, Sharjah, or a Free Zone, this blog will help you understand the most common bookkeeping pitfalls UAE businesses make — and, more importantly, how to avoid FTA penalties.

Let’s dive in.

Incomplete or Missing Financial Records

One of the biggest bookkeeping errors is failing to maintain complete transactional records. UAE law requires businesses to keep financial records, VAT invoices, returns, and supporting documents for at least five years — and up to seven or more in specific industries like real estate.

Why It Matters

Incomplete records:

⇒ Lead to disallowed VAT claims

⇒ Cause audit triggers

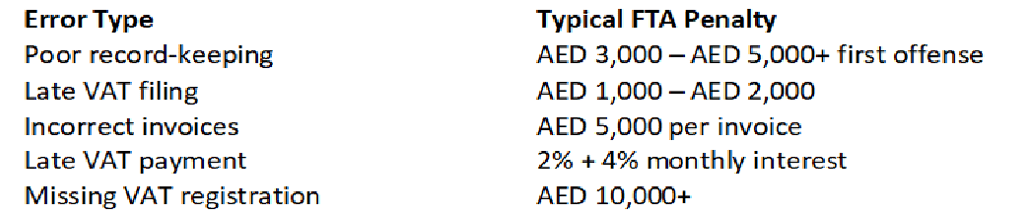

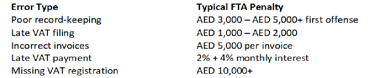

⇒ Result in fines (e.g., AED 3,000-AED 5,000 for poor record-keeping)

How to Avoid It

Use cloud-based bookkeeping (QuickBooks, Xero, Zoho) to store records

Create consistent naming conventions and folders for all invoices and receipts

Back up both digital and paper records regularly

Incorrect VAT Treatment & Classification

VAT compliance is a major bookkeeping concern. UAE businesses often:

Apply wrong VAT rates

Misclassify zero-rated or exempt supplies

Fail to apply reverse charge on imported services

These errors lead to inaccurate VAT returns and heavy penalties.

Example

Charging standard 5% VAT on a zero-rated export could result in underpaid VAT and penalties during an FTA audit.

How to Avoid It

Train staff on FTA VAT classification rules

Reconcile VAT accounts monthly

Use software with VAT-specific automation

Missing or Incorrect Tax Invoices

Every VAT-registered business in the UAE must issue compliant tax invoices. These must include:

Tax Registration Number (TRN)

VAT breakdown

Supplier details

Correct dates and numbering

Incorrect or missing invoices can attract AED 5,000 per non-compliant invoice.

How to Avoid It:

Standardise invoice templates

Validate invoices before sending

Integrate invoicing with your accounting system

Late VAT Filing & Payment

One of the most common FTA penalties arises from late VAT returns.

First late filing: AED 1,000

Repeat within 24 months: AED 2,000 or more

Late payment: escalating penalties up to 300% of unpaid tax

This is avoidable with proper bookkeeping discipline.

How to Avoid It

Set automated reminders in your accounting system

Maintain a tax calendar visible to all finance staff

Ensure VAT liabilities are calculated and paid before deadlines

Manual Errors & Non-Automated Bookkeeping

Many UAE SMEs still rely on manual spreadsheets or outdated systems — a recipe for errors and missing compliance cues. Manual processes:

Increase human error

Delay updates

Miss automated compliance checks

How to Avoid It

Switch to modern cloud accounting platforms

Use software that supports UAE tax rules

Enable automatic bank feeds and reconciliation

This drastically cuts errors and keeps your ledgers audit-ready.

Improper Bank Reconciliation

Bank reconciliation verifies that your books match your bank account — yet many businesses skip this step.

Why It’s Critical

Unreconciled books:

Mask cash flow issues

Cause discrepancies in VAT reporting

Leave unexplained adjustments during audits

How to Avoid It

Reconcile bank statements monthly

Investigate every discrepancy

Use automated reconciliation tools

Mixing Personal and Business Finances

Many small business owners use personal accounts for business expenses. This muddies your bookkeeping and increases audit risk.

How to Avoid It:

💳 Maintain a dedicated business account

💼 Separate personal expenses from business transactions

📊 Use corporate cards for employee expenses

Inadequate Cash Flow Tracking

Poor cash flow management leads to:

Missed VAT payments

Inability to settle liabilities on time

Untimely tax filings

This often results in penalties for non-payment.

How to Avoid It

Forecast cash flow weekly

Maintain sufficient VAT reserves

Automate alerts for upcoming tax payments

Failing to Track Accounts Payable and Receivable

Neglecting receivables and payables makes it harder to:

Reconcile financials

Know your taxable base

Prepare accurate financial reports

How to Avoid It

Review aged receivables monthly

Follow up on overdue invoices

Balance supplier invoices before tax filing

Unprepared for FTA Audits

Even error-free bookkeeping can be undermined by disorganisation. The FTA can audit your records at any time.

How to Stay Audit-Ready

Keep organised folders for each tax period

Maintain clear documentation trails

Conduct internal quarterly audits

Summary: Key Penalties & What Triggers Them

Best Practices for UAE Bookkeeping Compliance

To maintain accurate books and avoid FTA penalties:

1. Embrace Digital Accounting Tools

Cloud systems ensure accuracy and audit readiness.

2. Schedule Regular Reconciliations

Make reconciliation a monthly habit.

3. Automate VAT & Tax Alerts

Deploy tax calendars and automated reminders.

4. Train Your Team

Ensure finance staff understand UAE tax rules.

5. Annual Internal Reviews

Internal audits catch errors before the FTA does.

Why Professional Bookkeeping Services Matter

Bookkeeping isn’t just about numbers — it’s about compliance, readiness, and peace of mind. Outsourcing to a professional bookkeeping team ensures:

VAT accuracy

On-time filings

Audit-ready records

Peaceful relations with the FTA

Take Action: Avoid FTA Penalties Today

Don’t let bookkeeping mistakes cost you fines — or worse, disrupt your business operations. uae-bookkeeping.com specialises in UAE-compliant bookkeeping, VAT support, and audit readiness for businesses of all sizes.

Contact us now for a free consultation and get your books FTA-penalty-proof.

Start your compliance journey today!

© 2026 uae-bookkeeping.com