uae-bookkeeping.com

UAE Bookkeeping Requirements Explained (2026 Guide): Mainland vs Free Zone Businesses

UAE Bookkeeping Requirements Explained (2026 Guide): Mainland vs Free Zone Businesses

Gupta Group International

1/21/20265 min read

UAE Bookkeeping Requirements Explained (2026 Guide): Mainland vs Free Zone Businesses

Running a business in the United Arab Emirates (UAE) comes with tremendous benefits — from 0% tax regimes to world-class infrastructure and full foreign ownership in many jurisdictions. However, it also brings critical financial compliance obligations that every business must satisfy before they can fully enjoy these advantages.

In this comprehensive 2026 guide, we’ll unpack everything you need to know about bookkeeping requirements in the UAE, with a special focus on the differences between Mainland and Free Zone businesses. Whether you’re launching a new company, expanding in the UAE market, or simply looking to stay compliant, this article provides clear, actionable insights into what the law expects — and how proper bookkeeping can future-proof your business.

Why Bookkeeping Is Non-Negotiable in the UAE

From tax compliance to licensing and audit obligations, bookkeeping isn’t an optional admin task — it’s a legal requirement.

Under the UAE’s Commercial Companies Law, every registered company must maintain accurate financial records that reflect its financial transactions. These books must be retained for a significant period — at least five years from the end of the financial year.

But why does this matter?

Legal Compliance: You must maintain financial records that accurately reflect your company’s financial position and transactions as mandated by UAE law.

Tax Obligations: If your business is subject to VAT or Corporate Tax, you’ll need compliant bookkeeping to support returns, audits, and inspections.

Audit Requirements: Many businesses — especially larger ones or those in specific free zones — must prepare audited financial statements each year.

Bank & Investor Confidence: Banks and investors expect accurate records as a cornerstone of financial credibility.

Poor bookkeeping can result in fines, audit delays, rejected tax filings, and even license renewal issues. In extreme cases, it can jeopardize your business continuity.

Core Bookkeeping Requirements Across the UAE

Although specifics vary by jurisdiction, the UAE maintains several consistent bookkeeping principles:

1) Maintain Complete Accounting Records

All businesses must keep records that accurately reflect:

Sales and purchase invoices

Bank statements

Receipts and payment vouchers

Payroll and employee records

Ledger books and journals

Tax records and returns

These must be stored for a minimum of five years from the end of the fiscal year, while tax-related documents such as Corporate Tax documentation may need to be retained for up to seven years or more, especially where audits or disputes occur.

2) Follow Accepted Accounting Standards

Financial statements must generally be prepared in compliance with International Financial Reporting Standards (IFRS) or IFRS for SMEs where appropriate.

3) Prepare Annual Financial Statements

Most businesses — mainland and many free zones — must produce annual financial statements, including:

Balance sheet

Profit & loss statement

Cash flow statement

Notes to the accounts

These statements are essential for audits and tax computations

4) VAT Record Keeping

If your business is VAT-registered (mandatory when taxable supplies exceed AED 375,000 annually), you must retain:

VAT invoices

VAT returns

Supporting documentation

Minimum retention: typically 5 years.

5) Corporate Tax Readiness

With Corporate Tax active since June 2023, companies must keep records that substantiate tax computations and financials for at least seven years after the end of the tax period.

Mainland Companies: Requirements & Expectations

A Mainland business operates outside free zones and can conduct trade directly within the UAE market — without restrictions. While this brings opportunity, it also comes with more rigorous compliance.

1) Mandatory Audits

Mainland companies are generally required to have annual audits, often performed by auditors licensed by the Ministry of Economy. These audited financial statements must align with IFRS and be submitted according to regulatory timelines.

2) Longer Record Retention

Mainland businesses must retain records for at least seven years for tax purposes and five years for general accounting purposes.

3) Commercial Companies Law Compliance

Under Federal Decree-Law No. 32 of 2021, mainland companies must ensure books “accurately reflect” transactions and financial positions — a standard that auditors will enforce

Free Zone Companies: What’s Different?

Free zones are popular for their tax incentives, 100% foreign ownership, and simple setup procedures. But with benefits come administrative responsibilities — including bookkeeping.

1) Mandatory Bookkeeping

Although historically some free zones offered more flexibility, today all free zone companies must maintain accurate books of accounts. This ensures compliance with Corporate Tax and VAT laws and supports audit requirements where applicable.

2) Audit Requirements Vary by Zone

Some free zones — like DMCC, JAFZA, DAFZA, and RAKEZ — require annual audited financial statements as part of license renewal. Others may only require periodic financial statements without a mandatory audit, but this is increasingly rare.

3) Qualifying Free Zone Person (QFZP) Conditions

To enjoy 0% Corporate Tax benefits as a QFZP, companies must demonstrate:

Adequate substance in the free zone

No mainland UAE income

Compliance with accounting/reporting requirements

Failing these criteria can result in losing tax benefits and being taxed at 9%.

4) Record Retention and Reporting

The fundamentals remain the same: retain financial records for at least five years, prepare IFRS-compliant financials, and be ready for inspection by the Free Zone Authority or Federal Tax Authority upon request.

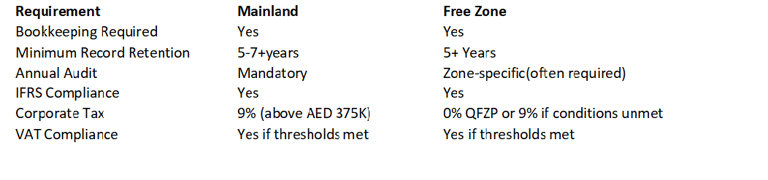

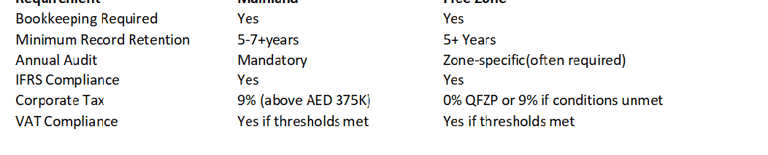

Mainland vs Free Zone — A Quick Comparison

Consequences of Non-Compliance

Failing to maintain accurate, compliant books can lead to:

Fines and penalties from FTA and authorities

Delays or denial in license renewals

Loss of free zone tax benefits

Difficulty opening or maintaining bank accounts

Audit challenges with local authorities

This reinforces that bookkeeping is not just an administrative task — it’s a foundation of financial health and legal compliance.

Practical Steps to Maintain Compliance

Here’s how UAE businesses can strengthen their bookkeeping processes:

1) Use Cloud Accounting Software

Tools like Xero, QuickBooks, and Zoho help automate entries, reconcile bank statements, and prepare VAT-ready data.

2) Schedule Monthly Reviews

Reconcile books monthly instead of waiting for year-end — it’s easier and keeps data audit-ready.

3) Hire Qualified Professionals

Certified accountants and bookkeeping experts understand local standards and ensure your reporting aligns with UAE laws.

4) Maintain Digital and Physical Records

Even with digital adoption, maintain organized backups of invoices, contracts, and statements for audits.

2026 Trends You Need to Watch

Looking ahead:

E-Invoicing Requirements: The UAE is enforcing digital invoicing from July 2026, underlining the shift toward automated, accurate financial records.

Mainland-Free Zone Integration: New policies allow free zone companies to operate more seamlessly on the mainland — but this requires dual bookkeeping clarity for income sources.

Corporate Tax Expansion: As more businesses enter the corporate tax regime, accurate books become non-negotiable for compliance and strategic tax planning.

Final Thoughts: Bookkeeping Is More Than Compliance — It’s Strategy

From tax readiness to bank credibility and strategic decision-making, bookkeeping is the backbone of your business’s financial integrity in the UAE.

Whether you operate on the Mainland or within a Free Zone, understanding your bookkeeping obligations is essential — not just for legal compliance, but for long-term success.

Take the Next Step With UAE-Bookkeeping.com

Are you ready to simplify your UAE bookkeeping process and stay compliant in 2026 and beyond?

Get a Consultation with our certified bookkeeping experts now

Request a Custom Bookkeeping Plan for Mainland or Free Zone

Download Our 2026 Compliance Checklist

📩 Contact us today at info@guptagroupinternational.com

or fill out the contact form on our website to start your compliance journey with confidence.

© 2026 uae-bookkeeping.com